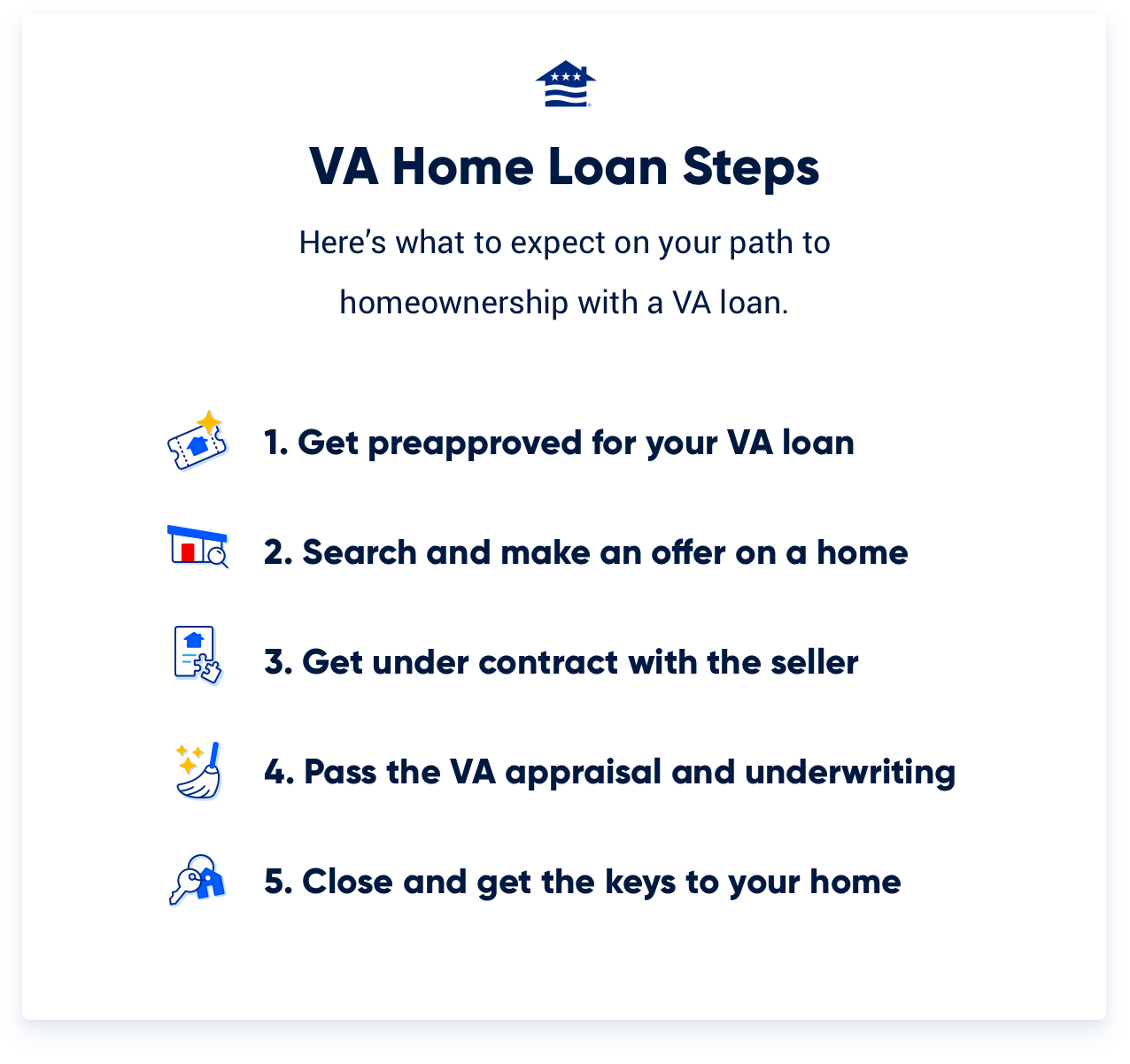

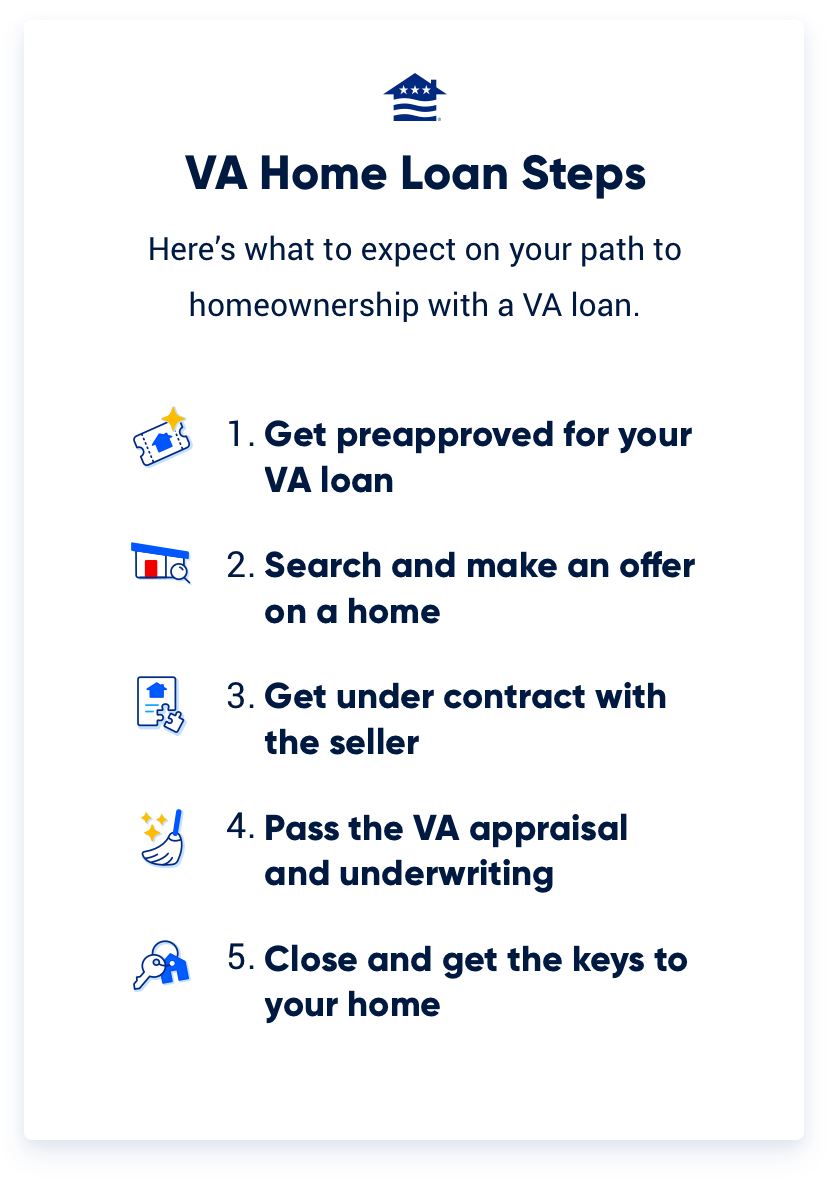

Getting a VA loan isn't significantly different from getting any other type of mortgage. For homebuyers, the VA loan has five basic steps: preapproval, house hunting, getting under contract, underwriting and closing.

This process typically results in a stronger financial future, using arguably the most powerful mortgage product on the market.

Here we detail the step-by-step process of getting a VA loan and how Veterans can get the most out of their VA loan benefit.

How to Buy a Home With a VA Loan

Understanding the full VA loan journey can help you move forward with more clarity and confidence. While the basic steps are similar to other mortgage types, VA loans have unique advantages and knowing what happens when can help you make the most of your benefit.

The visual below outlines the key milestones of the VA loan process, giving you a clear snapshot of what to expect from start to finish.

Now, let's walk through what each step involves and tips to help streamline the process.

Step 1: VA Loan Preapproval

Getting preapproved for a VA loan is a foundational first step. Preapproval is the initial green light from your mortgage lender and gives you a clear sense of your purchasing power.

Preapproval also adds weight to any offer you place on a home. In today's real estate environment, home sellers expect to see offers from preapproved buyers. Some sellers might not even consider your offer without a copy of your preapproval letter.

During preapproval, lenders assess your credit, finances, employment situation, service history and more. Lenders also validate your VA loan eligibility and service history with the Certificate of Eligibility (COE), which isn’t a document Veterans and service members need to get the process started.

Additional documents can include W-2s, recent pay stubs and bank statements. This step of the VA loan process can take minutes to hours, depending on your lender's documentation requirements.

At Veterans United, you can simply get preapproved for a VA loan online or through the MyVeteransUnited® mobile app in addition to a traditional phone call. Our mobile app allows you to easily upload documents and see all your loan details in one place.

Document requests can differ depending on the nature of your income, your military service history and more.

Documents You May Need to Provide During VA Loan Preapproval

- A copy of your driver's license or other government identification

- A copy of your DD-214 or Reserve/Guard points statements

- A statement of service for active duty borrowers

- Recent pay stubs and W-2s for the last two years

- Recent bank statements

- Disability award letters

Talk with your loan officer if you have questions about documentation needs. The faster you get this paperwork back to the lender, the quicker they can move to verify the information and finalize your loan preapproval.

Remember that a preapproval letter isn't a guarantee of financing, and this step is just the start of several to reach the final stage of the VA loan process.

Step 2: The House Hunt

With your preapproval letter in hand, you're ready to start the most exciting stage of the VA purchasing process – the house hunt.

Finding a real estate agent who truly knows VA loans is critical. These are more specialized home loan options, and some properties can be a better fit for VA loans than others. Plus, VA loans also offer big-time advantages when it comes to things like closing costs, and Veteran-friendly agents can help buyers get the most from their benefits.

Veterans United works to connect buyers with VA-savvy agents through Veterans United Realty, our national network of agents who understand the needs of military buyers.

Technically, you can look at houses before getting a preapproval, but it isn’t recommended. If you find a house you’re interested in, getting your preapproval may result in you putting in an offer too late or you might be misinformed about how much you could be preapproved for.

Additionally, your real estate agent will be able to help you find your ideal home better if they have a shared understanding of your preapproval amount.

VA Buyers Can Use Their Home Loan Benefit to Purchase

- Existing single-family homes

- New construction*

- Condos

- Manufactured and modular housing

- Multiunit properties

Like the other government-backed mortgage options, VA loans are for purchasing primary residences you intend to live in full time. Veterans can look to buy a multiunit property (up to a four-plex) as long as they plan to live in one of the units.

Homes generally need to be in good shape. The VA appraisal process includes a look at the home in light of some general property condition requirements, known as the Minimum Property Requirements (MPRs). MPRs are a high-level overview and not as in-depth as a home inspection. The VA doesn't require a home inspection, but home inspections are a key investment.

If the appraiser notes MPR issues, they may need to be resolved before the loan can close. VA buyers can ask sellers to pay for repairs and even cover the cost themselves if needed.

Purchasing a fixer-upper is possible with a VA loan, but the VA appraisal process can present challenges. Talk with a loan specialist in more detail if you're looking for that type of property.

Once you find a home you love, the next step is making an offer to buy it.

Step 3: Getting Under Contract

Your loan officer and a trusted real estate agent can help you craft a strong offer.

Your agent will look at recent comparable home sales in the area to help shape your starting point for a purchase price. Pricing and negotiation strategies can vary depending on the real estate market, the particular home and much more.

Veterans should discuss closing costs with their loan officer and agent before making an offer. VA loan closing costs can vary depending on a host of factors. Buyers can ask sellers to pay all their loan-related closing costs and up to 4% in concessions, which can cover escrow expenses and much more.

Most prospective VA buyers will present a contract with several contingencies that cover specific events leading up to the loan closing. Typical contingencies include the right to have a home inspection, handling repair requests, the number of days the buyer has to secure financing or the required earnest money deposit, which is a good-faith payment that demonstrates the buyer’s commitment to the purchase.

Every VA contract features added protection for the Veteran's earnest money regarding the VA appraisal. A special addendum ensures VA buyers get their earnest money back if the property's appraised value comes in low and the Veteran decides to back out of the deal.

It might take VA buyers a couple of rounds of negotiation to lock down a purchase agreement. Also, keep in mind that some markets are tougher than others. You may make offers on multiple homes before finding something that works. Every buyer-seller situation is different.

Step 4: Appraisal and Underwriting

The VA loan process jump-starts once you're under contract. Your loan team sends your contract and documentation to loan processors and underwriters to verify core financial and property information.

At this stage, the lender will also order the VA appraisal. Homebuyers typically cover the appraisal cost up front, although it's possible to seek a reimbursement from the seller at closing.

The VA assigns an independent, third-party appraiser to assess the property's value and condition. Lenders have no control over the appraiser, their timeline for conducting the appraisal or their assessment of the property.

The appraiser will look at recent comparable home sales when evaluating the home's fair market value. Buyers will need the home to appraise for at least what they've offered to pay for it. If an appraisal falls short, buyers will have to renegotiate with the seller, pay the difference in cash or move on to a different property.

If the appraiser notes repairs are needed to meet the VA's Minimum Property Requirements, buyers can ask the seller to pay for those or even cover the costs themselves in some cases.

Your loan team will likely have questions and requests for additional information while the appraisal process unfolds. The faster you get back to your lender with answers and information, the smoother this stage tends to go. Talk with your loan team if you have any questions or need an additional explanation about an underwriting request.

After passing the appraisal and VA underwriting, you'll receive a "clear to close," which means you're ready to head to your closing day. Being "clear to close" is still not a guarantee of financing, but you're just about there.

Step 5: Your VA Loan Closing

VA buyers will receive a Closing Disclosure shortly before their scheduled loan closing. This document allows buyers to compare their final closing costs and loan information to the estimates they received earlier in the process. Your loan officer typically reviews this document with you. Be sure to ask if you have any questions about your costs, fees or anything else.

You may also have a final walkthrough of the property. A final walkthrough allows you to verify any repairs, request removal for items you didn't want to stay behind and more. Contact your real estate agent and lender if there are any problems as soon as possible.

On closing day, expect to sign a lot of paperwork and finally get the keys to your new home.

A good understanding of the VA loan process will help you get the most from your budget and this incredibly powerful benefit. Talk with a Veterans United Home Loan specialist to kickstart your homebuying journey.

1 Our military advisors are paid employees of Veterans United Home Loans.